The Tories introduced the 50% strike ballot threshold to make industrial action harder. MATT WRACK argues that a Labour government has no justification for leaving it on the statute book

The coming cashless dystopia?

Tapping with your phone, using chip and pin, paying online — it all seems so much easier than notes and coins. But nothing pushed by big tech and the financial industry giants is in our favour, argues JOHN GREEN

In the wake of Ann Widdecombe’s murder, JOHN GREEN wonders whether the government will really get to grips with the root cause of these attacks on our MPs

The new PM’s opening addresses offered hope, council homes and reform — but little detail on how any of it will be delivered, warns CLAUDIA WEBBE

Despite the screeching from the right-wing media, Burnham’s speech chimed with the public mood - and socialists should take advantage, says Morning Star editor BEN CHACKO

Scotland's Labour leader cannot continue to evade responsibility for the party's decline, argues LAUREN HARPER

Nature as well as society works dialectically, asserts the Marx Memorial Library and Workers’ School

MANY readers will already have experienced situations where they are unable to pay for things in cash and have to use a valid credit or debit card. Car parking is only one such transaction where having a card is almost obligatory these days, most supermarkets are changing their checkouts to cashless machines — and the new Amazon grocery shops don’t take cash at all. Many of us are now mostly shopping online and credit and debit cards are obligatory.

Even our relationship with government agencies and local authorities is now almost impossible without access to a computer and a credit card. What’s wrong with that, you might ask? If you’ve got a good credit rating and bank account, you may prefer the idea of paying by card — it’s simple and painless and you don’t have to carry a wad of cash and small change in your pocket.

We see headlines in the press, like “Customers move towards digital payments” and “Banks shutting down ATMs as people move towards digital payments” — as if everyone is just collectively acting like this, and the big institutions are just following our lead.

Similar stories

Ron's rages are sincere and — according to his wife — healthily cathartic. But can these splenetic outbursts loosen the grip of capitalism at its most monstrous?

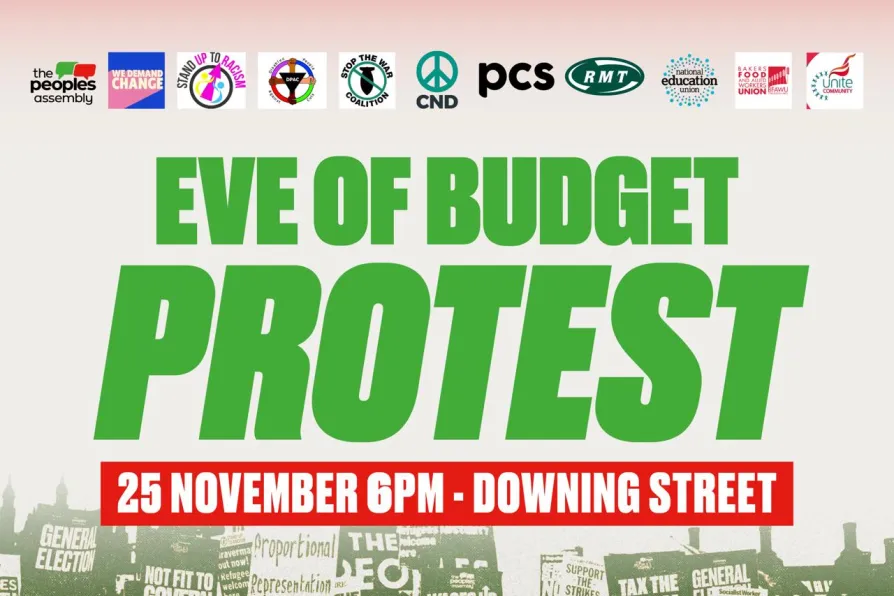

Austerity in a red tie is still austerity, warns RAMONA McCARTNEY of the People’s Assembly – rally with us to demand different choices

Digital ID means the government could track anyone and then limit their speech, movements, finances — and it could get this all wrong, identifying the wrong people for the wrong reasons, as the numerous digital cockups so far demonstrate, warns DYLAN MURPHY